Section 149(3) of the

Companies Act, 2013 Hampers the flow of FDI into India

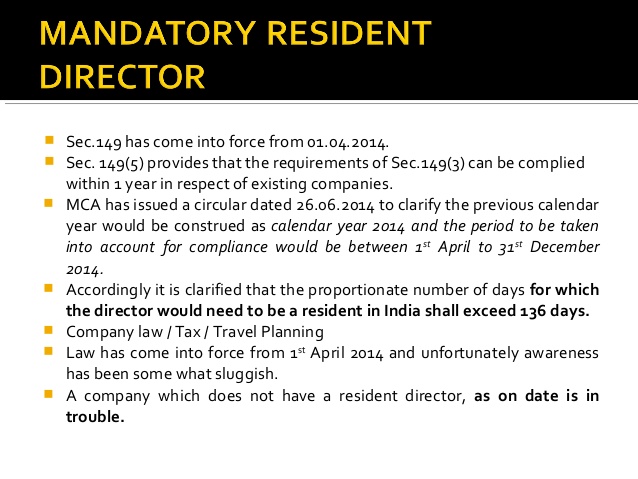

Through its General Circular No. 2Sl2O14-No. I/22/|3-CL, V

dated 266 June. 2O14 , MCA has clarified that at least one director of a

company has to stay in India for a total period oi not less than 182 days in

the previous calendar year under Section 149(3) of the Companies Act, 2013

(Act).

Section 149(3) of the Companies Act, 2013 (Act) requires

every company to have at least one director who has stayed in India for a total

period of not less than 182 days in the previous calendar year.

Government has received many requests from stakeholders for

clarification with regard to applicability of these provisions in the current

calendar/financial year as there is an ambiguity in the definition.

2. As per the above circular , MCA has clarified that the,

residency requirement' would be reckoned from the date of commencement of

section 149 of the Act i.e. 1st April, 2014, The first, previous calendar year,

for compliance with these provisions would, therefore, be Calendar year 2014.

The period to be taken into account for compliance with these provisions will

be the remaining period of calendar year 2014 i.e. 1st April to 31"1

December). Therefore, on a proportionate basis, the number of days for which

the director(s) would need to be resident in India during Calendar year.2014,

shall exceed 136 days.

Regarding newly incorporated companies, it is claimed that

companies incorporated between 1.4.2014 to 3O.9.2O14 should have a resident

director either at the incorporation stage itself or within six months of their

incorporation. Companies incorporated after 30.9.2014 need to have the resident

director from the date of incorporation itself.

Thus, it is submitted that Section 149(3) of the Companies

Act, 2013 hampers the flow of foreign investment into India

.

Companies formed with 100% equity held by

foreign citizens or non-resident Indians or PIOs should be allowed to act as

the directors of the company irrespective of the fact whether they stayed in

India for a minimum period of 182 days in the previous calendar year or not.

After all, day to day affairs of the company can be managed

by CEO or COO or CFO or Company Secretary or manager in India and these persons

can be appointed as key managerial person (KMP) and will be accountable for the

actions of the company in India.

Since Modi Government is giving prime importance to “Make In

India “and allows 100% FDI in Defence, Airports etc, it is submitted that the section 149 (3) Act is superfluous and

there is an immediate necessity to amend the Act allowing foreign investors to

be remain as directors of the Company irrespective of the fact whether they

remain in India for 182 days or not.

Section 167 of the Companies Act of 2013 also impedes the

flow of FDI into India.

Under section 167 of the Companies Act of 2013 (‘2013 Act’)

sub-section (b) states that if he absents himself from all the meetings of the

Board of Directors held during a period of twelve months with or without

seeking leave of absence of the Board; he is deemed to have vacated his office.

Section 167 (1) (b) states that if a director fails to

participate in the board for a period of twelve months or more, with or without the leave of the Board, he

shall be deemed to have vacated his office.

In other words, we can

say Section 167 of CA

2013 states that a director (non-resident or non-resident Indian director)

shall have to attend one Board Meeting in India compulsorily with his physical presence.

However, the Board Meeting attended by

any Director, whether in person or through video conferencing or other audio

visual means, shall be sufficient attendance for the purpose of section

167(1)(b).

Section 173 (2) of the Companies Act

2013 states that a director of a company can participate in the board meeting

of a company either in person or through video-conferencing or through other

audio visual means , shall be construed as he participated the meeting as per

law and his presence will be held for the quorum.

Further , section 149 (3) of the CA 2013 is silent what repercussion would

come if both directors of a company stays outside India more than 182 days.

Hence section 149(3) of the Companies Act, 2013 (Act) has

become redundant due to section 173 (2) of the Companies Act.

Hence , it is submitted that MCA should issue a circular or

removal of doubt that that there is no need for a foreign or a NRI director to

be present in India physically for a period of 182 days in virtue of section173

(2) of the Companies Act.

An early action of the subject will facilitate more FDI flows

into India.

PMO HAS ACCEPTED ONE OF MY SUGGESTION

PMO HAS ACCEPTED ONE OF MY SUGGESTION

PMO has now accepted part of my suggestion and informed me that section 149 (3) is going to be amended through the Companies (Amendment) Bill, 2016 to provide that instead of applicability of this requirement for previous calendar year, the current financial year is being proposed.

I really wish to thank both PMO office and Ministry of Corporate Affairs to accept the view of a professional. This demonstrates that Modi government is hearing the suggestion of ordinary citizen. There is no wonder why India is now jumped 15 place ahead in doing business on the International level.

I thank PM Modi ji and Ministry of Corporate Affairs for accepting one of my views in the Companies Amendment Bill, 2016.

No comments:

Post a Comment